What To Look For From This Week’s Fed Meeting

You may be hearing a lot of talk about the Federal Reserve (the Fed) and how their actions will impact the housing market right now. Here’s why. The Fed meets again this week to decide the next step with the Federal Funds Rate. That's how much it costs banks to borrow from each other. Now, that’s not the same thing as setting mortgage rates, but mortgage rates can be influenced through this process. And if you’re thinking about buying or selling a home, you may be wondering about the downstream impact and when mortgage rates will come down. Here’s a quick rundown of what you need to know to help you anticipate what’ll happen next. The Fed’s decisions are guided by these three key economic indicators: The Direction of Inflation How Many Jobs the Economy Is Adding The Unemployment Rate Let’s take a look at each one. 1. The Direction of Inflation You’ve likely noticed prices for everyday goods and services seem to be higher each time you make a purchase at the store. That’s because of inflation – and the Fed wants to see that number come back down so it’s closer to their 2% target. Right now, it’s still higher than that. But despite a little volatility, inflation has generally been moving in the right direction. It gradually came down over the past two years, and is holding fairly steady right now (see graph below): The path of inflation – though still not at their target rate – is a big part of the reason why the Fed will likely lower the Fed Funds Rate again this week to make borrowing less expensive, while still ensuring the economy continues to grow. 2. How Many Jobs the Economy Is Adding The Fed is also keeping an eye on how many new jobs are added to the economy each month. They want job growth to slow down a bit before they cut the Federal Funds Rate further. When fewer jobs are created, it shows the economy is still doing well, but gradually cooling off—exactly what they’re aiming for. And that’s what’s happening right now. Reuters says: “Any doubts the Federal Reserve will go ahead with an interest-rate cut . . . fell away on Friday after a government report showed U.S. employers added fewer workers in October than in any month since December 2020.” Employers are still hiring, but just not as many positions right now. This shows the job market is starting to slow down after running hot for a while, which is what the Fed wants to see. 3. The Unemployment Rate The unemployment rate shows the percentage of people who want jobs but can’t find them. A low unemployment rate means most people are working, which is great. However, it can push inflation higher because more people working means more spending—and that makes prices go up. Many economists consider any unemployment rate below 5% to be as close to full employment as is realistically possible. In the most recent report, unemployment is sitting at 4.1% (see graph below): Unemployment this low shows the labor market is still strong even as fewer jobs were added to the economy. That’s the balance the Fed is looking for. What Does This Mean Going Forward? Overall, the economy is headed in the direction the Fed wants to see – and that’s why experts say they will likely cut the Federal Funds Rate by a quarter of a percentage point this week, according to the CME FedWatch Tool. If that expectation ends up being correct, that could pave the way for mortgage rates to come down too. But that doesn’t mean they’ll fall immediately. It will take some time. Remember, the Fed doesn’t determine mortgage rates. Forecasts show mortgage rates will ease more gradually over the course of the next year as long as these economic indicators continue to move in the right direction and the Fed can continue their Federal Funds rate cuts through 2025. But a change in any one of the factors mentioned here could cause a shift in the market and in the Fed’s actions in the days and months ahead. So, brace for some volatility, and for mortgage rates to respond along the way. As Ralph McLaughlin, Senior Economist at Realtor.com, notes: "The trajectory of rates over the coming months will be largely dependent on three key factors: (1) the performance of the labor market, (2) the outcome of the presidential election, and (3) any possible reemergence of inflationary pressure. While volatility has been the theme of mortgage rates over the past several months, we expect stability to reemerge towards the end of November and into early December." Bottom Line While the Fed’s actions play a part, economic data and market conditions are what really drive mortgage rates. As we move through the rest of 2024 and 2025, expect rates to stabilize or decline gradually, offering more certainty in what has been a volatile market.

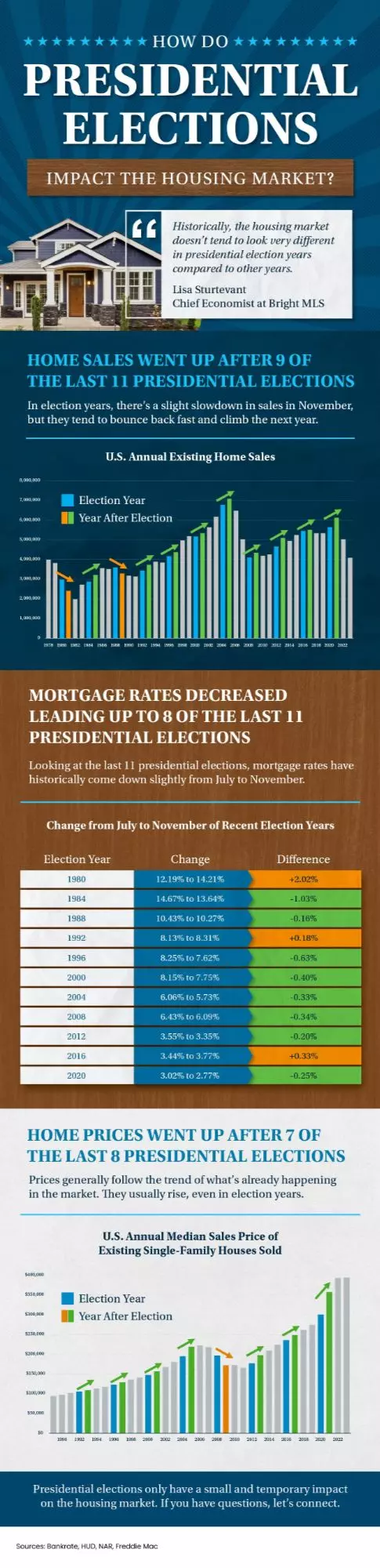

Read MoreQ&A: How Do Presidential Elections Impact the Housing Market?

Even if you’re not looking to move right away, you may have questions about how the election will impact the housing market. When we look at historical trends, combined with what’s happening right now, we can find your answers. Based on historical data, mortgage rates decrease in the months before and home prices and sales increase the year after the election. The facts show Presidential elections only have a small and temporary impact on the housing market.

Read MoreWhy Today’s Foreclosure Numbers Won’t Trigger a Crash

With everything feeling more expensive these days, it’s natural to worry about how rising costs might impact the housing market. Many people are concerned that high prices and tighter budgets could cause more homeowners to fall behind on their mortgage payments, leading to a wave of foreclosures. But before you start worrying about a housing market crash, here’s a look at what’s really happening. And the good news is: the latest foreclosure data shows there’s no wave on the horizon. How Today’s Market Is Different from 2008 Let’s ease those fears by looking at the bigger picture. The graph below uses research from ATTOM, a property data provider, to show that the number of homeowners starting the foreclosure process is nowhere near what we saw coming out of 2008. Back then, there was a big spike in how many foreclosures were happening. Today, the number is much lower – it's even dropped some in the latest report. There’s a big difference between what’s happening now, and what happened when the housing market crashed (see graph below): Just in case you’re wondering why the number of foreclosure filings has ticked up slightly since 2020 and 2021, here’s what you need to know. During those years, there was a moratorium (shown in white) designed to help millions of homeowners avoid foreclosure in challenging times. That’s why the numbers for just a few years ago were so incredibly low. If you look further back, it’s clear overall foreclosure filings are down significantly. And if you’re wondering: how are there fewer foreclosures today, even when the cost of living has gotten so pricey? Here’s your answer. One of the main reasons is that homeowners today have a lot more equity built up in their homes than they did back in 2008. As an article from Bankrate explains: “In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.” This equity acts like a safety net and is allowing many homeowners to avoid going into foreclosure if they’re facing financial hardships. Even if someone is struggling to make their monthly payments, they may be able to sell their home and avoid foreclosure altogether. This is a far cry from the conditions during the crash when homeowners owed more on their mortgages than their homes were worth. What’s Ahead for the Housing Market It’s true that today’s higher cost of living across the board is a challenge for many people right now. But this doesn’t mean we’re heading for a surge in foreclosures. The equity cushion that people have is helping to keep foreclosure filings low. Today’s homeowners have more options to avoid going into foreclosure. Bottom Line Yes, everyday costs for gas and food have gotten more expensive—but that doesn’t mean the housing market is on the brink of another foreclosure crisis. Data shows the market is far from a foreclosure wave. Homeowners today are in a much stronger financial position than they were during the 2008 crash, thanks to significant equity.

Read MoreWhy Home Sales Bounce Back After Presidential Elections

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down. Election Years Bring a Temporary Slowdown In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day (see graph below): Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it's particularly apparent for buyers and sellers in the housing market. This year is no different. A recent survey from Redfin found that 23% of potential first-time homebuyers said they’re waiting until after the election to buy. That’s nearly a quarter of first-time buyers hitting the pause button, likely due to the same feelings of uncertainty. Home Sales Bounce Back After the Election The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election (see chart below): That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales. What To Expect in 2025 If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. As the graph below shows, the housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year (see graph below): And that aligns with the typical pattern of post-election rebounds. So, while it might feel like the market is slowing down right now, it’s more of a temporary dip rather than a long-term trend. As has been the case before, once the election uncertainty passes, buyers and sellers will return to the market. Bottom Line It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.

Read MoreTwo Reasons Why the Housing Market Won’t Crash

You may have heard chatter recently about the economy and talk about a possible recession. It's no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now. Real estate journalist Michele Lerner says: “A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.” With that definition in mind, here are two reasons why this just isn’t on the horizon. 1. Demand for Homes Is Higher than Supply One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story. It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context: The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today. Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash. It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says: “We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.” 2. Unemployment Is Still Low When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below): Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%. Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices. Today’s Housing Market Is Stronger than in 2008 While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company: “Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.” Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon. Bottom Line The housing market is doing a lot better than it was in 2008, but it’s important to remember that real estate is very local. So, it’s always a good idea to stay informed about our specific market. If you have any questions or want to discuss how these factors are playing out in our area, feel free to reach out.

Read MoreWhat's the Impact of Presidential Elections on the Housing Market?

It’s no surprise that the upcoming Presidential election might have you speculating about what’s ahead. And those unanswered thoughts can quickly spiral, causing fear and uncertainty to swirl through your mind. So, if you’ve been considering buying or selling a home this year, you’re probably curious about what the election might mean for the housing market – and if it’s still a good time to make your move. Here’s the good news that may surprise you: typically, Presidential elections have only had a small, temporary impact on the housing market. But your questions are definitely worth answering, so you don’t have to pause your plans in the meantime. Here’s a look at decades of data that shows exactly what’s happened to home sales, prices, and mortgage rates in previous Presidential election cycles, so you can move forward with the facts as you weigh the pros and cons of your homeownership decision. Home Sales In the month leading up to a Presidential election, from October to November, there’s typically a slight slowdown in home sales (see graph below): Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary. Historically, home sales bounce right back and continue to rise the following year. In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after 9 of the last 11 Presidential elections, home sales went up the year after the election, and it’s been happening consistently since the early 1990s (see chart below): Home Prices You may also be wondering about home prices. Do prices come down during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist notes: “An election year doesn’t alter the price trend that is already happening in the market.” Home prices generally rise over time, regardless of an election cycle. So, based on what history shows, you can expect the current pricing trend in your local market to likely continue, barring any unusual market or economic circumstances. The latest data from NAR reveals that after 7 of the last 8 Presidential elections, home prices increased the following year (see chart below): The one outlier was from 2008 to 2009, which was during the height of the housing market crash. That was certainly not a typical year. Today’s market, however, is much more resilient. And while prices are moderating nationally, they aren’t on an overall decline. Mortgage Rates And the third thing that’s likely on your mind is mortgage rates, since they impact your monthly payment if you’re financing a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in 8 of them (see chart below): And this year, we’ve already started to see that happen. Most experts also forecast mortgage rates will ease slightly throughout the rest of 2024. If that happens – and all signs right now indicate it should – this year will continue to follow the trend of declining rates. So, if you’re looking to buy a home in the coming months, this could be great news for your purchasing power. What This Means for You What’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually minimal. As Lisa Sturtevant, Chief Economist at Bright MLS, says: “Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.” For most buyers and sellers, elections don’t have a major impact on their plans. Bottom Line While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. And this means you don’t have to pause your plans in the meantime. For help navigating the market during this election cycle, let’s connect.

Read MoreToday’s Biggest Housing Market Myths

Have you ever heard the phrase: don’t believe everything you hear? That’s especially true if you’re thinking about buying or selling a home in today’s housing market. There’s a lot of misinformation out there. And right now, making sure you have someone you can go to for trustworthy information is extra important. If you partner with a real estate agent, they can clear up some common misconceptions and reassure you by backing them up with research-driven facts. Here are just a few misconceptions they can help disprove. 1. I’ll Get a Better Deal Once Prices Crash If you’ve heard home prices are going to come crashing down, it’s time to look at what’s actually happening. While prices vary by local market, there’s a lot of data out there from numerous sources that shows a crash is not going to happen. Back in 2008, there was a dramatic oversupply of homes that led to prices crashing. Across the board, there’s an undersupply of homes for sale today. That makes this market a whole different scenario (see chart below): So, if you think waiting will score you a deal, know that data shows there’s not a crash on the horizon, and waiting isn’t going to pay off the way you’d hoped. 2. I Won’t Be Able To Find Anything To Buy If this nagging fear about finding the right home if you move is still holding you back, you probably haven’t talked with an expert real estate agent lately. Throughout the year, the supply of homes for sale has grown. Data from Realtor.com helps put this into context. While there are still fewer homes on the market than in a more normal year like 2019, inventory is still above where it was at this time last year (see graph below): So, if you’re remembering all that media coverage about record-low supply during the pandemic, you can rest a bit easier. While the market isn’t back to normal just yet, inventory is moving in a healthier direction. And that means as your options improve, you can let go of this now outdated myth because finding a home to buy won’t feel quite so impossible anymore. 3. I Have To Wait Until I Have Enough for a 20% Down Payment Many people still believe you need a 20% down payment to buy a home. To show just how widespread this myth is, Fannie Mae says: “Approximately 90% of consumers overstate or don’t know the minimum required down payment for a typical mortgage.” And if you look at the data from the National Association of Realtors (NAR), you can see the typical homeowner isn’t putting down as much as you might expect (see graph below): First-time homebuyers are typically only putting down 6%. That’s far less than the 20% so many people think they need. And if you’re looking at that graph and you’re more focused on how the number for repeat buyers is closer to 20%, here’s what you need to realize. That’s only because they have so much equity built up in their current house that can be used to make a larger down payment for their next move. This goes to show you don’t have to put 20% down, unless it’s specified by your loan type or lender. Many people put down a lot less. Not to mention, depending on the type of home loan you get, you may only need to put 3.5% or even 0% down. So, if you’re buying your first home, you likely don’t need nearly as much for your down payment as you may think. An Agent’s Role in Fighting Misconceptions If you put your move on pause because you heard one or more of these myths yourself, it’s time to talk to a trusted agent. An expert agent has more data and the facts, just like this, to reassure you and help break through any misconceptions that may be holding you back. Bottom Line If you have questions about what you’re hearing or reading, let’s connect. You deserve to have someone you can trust to get the facts.

Read MoreThe Great Wealth Transfer: A New Era of Opportunity

In recent years, there’s been a significant shift in how wealth is distributed among generations. It’s called the Great Wealth Transfer. Historically, the transfer of wealth from one generation to the next was a more gradual process, often limited to smaller amounts of inheritance or family savings. But today, the scale has increased in a big way. As a recent article from Bankrate says: “The biggest wave of wealth in history is about to pass from Baby Boomers over the next 20 years, and it’s going to have major impacts on many facets of life. Called The Great Wealth Transfer, $84 trillion is poised to move from older Americans to Gen X and millennials. If it’s managed smartly, Americans will be able to grow their wealth and ensure their financial security.” Basically, as more Baby Boomers retire, sell businesses, or downsize their homes, more substantial assets are being passed down to younger generations. And this creates a powerful ripple effect that’ll continue over the next few decades. The graph below uses data from Merrill and Cerulli Associates to give you an idea of how much inherited money is set to change hands through 2045: Impact on the Housing Market One of the most immediate effects of this wealth transfer is on the housing market. Home affordability has been a concern for many aspiring buyers, especially in high-demand areas. The increase in generational wealth is expected to ease some of these challenges by providing future homeowners with greater financial resources. As assets are passed down through generations, buyers may find themselves in a better position to afford homes. Merrill talks about that benefit in a recent article: “While millennials face steep barriers . . . to buying a first home in many markets, ‘that’s a for-now story, not a forever story’ . . . The Great Wealth Transfer should enable more of them to become homeowners — or trade up or add a second home — either through inherited property or the funds for a down payment.” Impact on the Economy But the Great Wealth Transfer doesn’t just impact housing. It’s also going to provide a new avenue for entrepreneurial spirits to fuel economic growth. If someone is looking to start a business and they’re receiving funds like this, that money can used as the necessary capital to start a new company. This helps the next generation of innovators and business owners bring their ideas to life. Bottom Line While affordability remains a challenge in today’s housing market, the ongoing Great Wealth Transfer is poised to unlock new opportunities. As wealth is passed down and put to use, it’s expected to ease some of the barriers to homeownership and fuel other entrepreneurial endeavors.

Read MoreIs Affordability Starting To Improve?

Over the past couple of years, a lot of people have had a hard time buying a home. And while affordability is still tight, there are signs it's getting a little better and might keep improving throughout the rest of the year. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says: “Housing affordability is improving ever so modestly, but it is moving in the right direction.” Here’s a look at the latest data on the three biggest factors affecting home affordability: mortgage rates, home prices, and wages. 1. Mortgage Rates Mortgage rates have been volatile this year, bouncing around from the mid-6% to low 7% range. But there's some good news. Data from Freddie Mac shows rates have been trending down overall since May (see graph below): Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down. Even a small drop can help you out. When rates decline, it's easier to afford the home you want because your monthly payment will be lower. Just don’t expect them to go back down to 3%. 2. Home Prices The second big thing to think about is home prices. Nationally, they’re still going up this year, but not as fast as they did a couple of years ago. The graph below uses home price data from Case-Shiller to illustrate that point: If you're thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says: “While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help – so the dream of homeownership isn’t boarded up just yet.” 3. Wages Another factor helping with affordability is rising wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have increased over time: Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you'll see wages are rising even faster than normal right now – that's the green line. This helps you because if your income increases, it's easier to afford a home. That’s because you won't have to spend as much of your paycheck on your monthly mortgage payment. Bottom Line When you put all these factors together, you see mortgage rates are trending down, home prices are rising more slowly, and wages are going up faster than usual. Though affordability is still a challenge, these trends are early signs things might be starting to improve.

Read MoreMortgage Rates Down a Full Percent from Recent High

Mortgage rates have been one of the hottest topics in the housing market lately because of their impact on affordability. And if you’re someone who’s looking to make a move, you’ve probably been waiting eagerly for rates to come down for that very reason. Well, if the past few weeks are any indication, you may be getting your wish. Mortgage Rates Trend Down in Recent Weeks There’s big news for mortgage rates. After the latest reports on the economy, inflation, the unemployment rate, and the Federal Reserve’s recent comments, mortgage rates started dropping a bit. And according to Freddie Mac, they’re now at a level we haven’t seen since February. To help show the downward trend, check out the graph below: Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says: “The hopes for lower interest rates need the reality check that 'lower' doesn't mean we're going back to 3% mortgage rates. . . the best we may be able to hope for over the next year is 5.5 to 6%.” And with the decrease in recent weeks, you’ve got a big opportunity in front of you right now. It may be enough for you to want to jump back in. The Relationship Between Rates and Demand If you wait for mortgage rates to drop further, you might find yourself dealing with more competition as other buyers re-ignite their home searches too. In the housing market, there’s generally a relationship between mortgage rates and buyer demand. Typically, the higher rates are, the lower buyer demand is. But when rates start to come down, things change. Buyers who were on the fence over higher rates will resume their searches. Here’s what that means for you. As a recent article from Bankrate says: “If you’re ready to buy, now might be the time to strike. Home prices have been rising primarily because of a longstanding shortage of homes for sale. That’s unlikely to change, and if mortgage rates do fall below 6%, it’s possible buyers would enter the market en masse, further pushing up prices and resurrecting bidding wars.” Bottom Line If you’ve been waiting to make your move, the recent downward trend in mortgage rates may be enough to get you off the sidelines. Rates have hit their lowest point in months, and that gives you the opportunity to jump back in before all the other buyers do too. If you’re ready and able to start the process, reach out and let’s get started.

Read MoreHow the Economy Impacts Mortgage Rates

As someone who’s thinking about buying or selling a home, you’re probably paying close attention to mortgage rates – and wondering what's ahead. One thing that can affect mortgage rates is the Federal Funds Rate, which influences how much it costs banks to borrow money from each other. While the Federal Reserve (the Fed) doesn’t directly control mortgage rates, they do control the Federal Funds Rate. The relationship between the two is why people have been watching closely to see when the Fed might lower the Federal Funds Rate. Whenever they do, that’ll put downward pressure on mortgage rates. The Fed meets next week, and three of the most important metrics they’ll look at as they make their decision are: The Rate of Inflation How Many Jobs the Economy Is Adding The Unemployment Rate Here’s the latest data on all three. 1. The Rate of Inflation You’ve probably heard a lot about inflation over the past year or two – and you’ve likely felt it whenever you’ve gone to buy just about anything. That’s because high inflation means prices have been going up quickly. The Fed has stated its goal is to get the rate of inflation back down to 2%. Right now, it’s still higher than that, but moving in the right direction (see graph below): 2. How Many Jobs the Economy Is Adding The Fed is also watching how many new jobs are created each month. They want to see job growth slow down consistently before taking any action on the Federal Funds Rate. If fewer jobs are created, it means the economy is still strong but cooling a bit – which is their goal. That appears to be exactly what’s happening now. Inman says: “. . . the Bureau of Labor Statistics reported that employers added fewer jobs in April and May than previously thought and that hiring by private companies was sluggish in June.” So, while employers are still adding jobs, they’re not adding as many as before. That’s an indicator the economy is slowing down after being overheated for quite some time. This is an encouraging trend for the Fed to see. 3. The Unemployment Rate The unemployment rate is the percentage of people who want to work but can’t find jobs. So, a low rate means a lot of Americans are employed. That’s a good thing for many people. But it can also lead to higher inflation because more people working means more spending – which drives up prices. Right now, the unemployment rate is low, but it’s been rising slowly over the past few months (see graph below): It may seem harsh, but a consistently rising unemployment rate is something the Fed needs to see before deciding to cut the Federal Funds Rate. That’s because a higher unemployment rate would mean reduced spending, and that would help get inflation back under control. What Does This Mean Moving Forward? While mortgage rates are going to continue to be volatile in the days and months ahead, these are signs the economy is headed in the direction the Fed wants to see. But even with that, it’s unlikely they'll cut the Federal Funds Rate when they meet next week. Jerome Powell, Chair of the Federal Reserve, recently said: “We want to be more confident that inflation is moving sustainably down toward 2% before we start the process of reducing or loosening policy.” Basically, we’re seeing the first signs now, but they need more data and more time to feel confident that this is a consistent trend. Assuming that direction continues, according to the CME FedWatch Tool, experts say there’s a projected 96.1% chance the Fed will lower the Federal Funds Rate at their September meeting. Remember, the Fed doesn’t directly set mortgage rates. It’s just that whenever they decide to cut the Federal Funds Rate, mortgage rates should respond. Of course, the timing of when the Fed takes action could change because of new economic reports, world events, and other factors. That’s why it's usually not a good idea to try to time the market. Bottom Line Recent economic data may signal that hope is on the horizon for mortgage rates. Let’s connect so you have an expert to keep you up to date on the latest trends and what they mean for you.

Read MoreHow Do Presidential Elections Impact the Housing Market?

Are you wondering if the upcoming election will have an impact on the housing market? Here’s what history tells us you need to know if you’re considering a move. Data shows home sales slow in November but quickly bounce back and rise the following year. Prices usually keep climbing. And mortgage rates typically come down slightly. Presidential elections have only a small and temporary impact on the housing market. If you have questions, let’s connect.

Read MoreNot a Crash: 3 Graphs That Show How Today’s Inventory Differs from 2008

Even if you didn't own a home at the time, you probably remember the housing crisis in 2008. That crash impacted the lives of countless people, and many now live with the worry that something like that could happen again. But rest easy, because things are different than they were back then. As Business Insider says: “Though many Americans believe the housing market is at risk of crashing, the economists who study housing market conditions overwhelmingly do not expect a crash in 2024 or beyond.” Here’s why experts are so confident. For the market (and home prices) to crash, there would have to be too many houses for sale, but the data doesn't show that’s happening. Right now, there’s an undersupply, not an oversupply like the last time – and that’s true even with the inventory growth we’ve seen this year. You see, the housing supply comes from three main sources: Homeowners deciding to sell their houses (existing homes) New home construction (newly built homes) Distressed properties (foreclosures or short sales) And if we look at those three main sources of inventory, you’ll see it’s clear this isn’t like 2008. Homeowners Deciding To Sell Their Houses Although the supply of existing (previously owned) homes is up compared to this time last year, it’s still low overall. And while this varies by local market, nationally, the current months’ supply is well below the norm, and even further below what we saw during the crash. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), we only have about a third of that available inventory today. So, what does this mean? There just aren't enough homes available to make values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that's not the case right now. New Home Construction People are also talking a lot about what's going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. Even though new homes make up a larger percentage of the total inventory than the norm, there’s no need for alarm. Here’s why. The graph below uses data from the Census to show the number of new houses built over the last 52 years. The orange on the graph shows the overbuilding that happened in the lead-up to the crash. And, if you look at the red in the graph, you’ll see that builders have been underbuilding pretty consistently since then: There’s just too much of a gap to make up. Builders aren’t overbuilding today, they’re catching up. A recent article from Bankrate says: “What’s more, builders remember the Great Recession all too well, and they’ve been cautious about their pace of construction. The result is an ongoing shortage of homes for sale.” Distressed Properties (Foreclosures and Short Sales) The last place inventory can come from is distressed properties, including short sales and foreclosures. During the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford. Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from ATTOM to show how things have changed since the housing crash: This graph makes it clear that as lending standards got tighter and buyers became more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures (shown in black) and the forbearance program helped prevent a repeat of the wave of foreclosures we saw when the market crashed. While you may see headlines that foreclosure volume is ticking up – remember, that’s only compared to recent years when very few foreclosures happened. We’re still below the normal level we’d see in a typical year. What This Means for You Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. As Forbes explains: “As already-high home prices continue trending upward, you may be concerned that we’re in a bubble ready to pop. However, the likelihood of a housing market crash—a rapid drop in unsustainably high home prices due to waning demand—remains low for 2024.” Mark Fleming, Chief Economist at First American, points to the laws of supply and demand as a reason why we aren't headed for a crash: “There’s just generally not enough supply. There are more people than housing inventory. It’s Econ 101.” And Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says: “We will not have a repeat of the 2008–2012 housing market crash. There are no risky subprime mortgages that could implode, nor the combination of a massive oversupply and overproduction of homes.” Bottom Line The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing experts and inventory data tell us there isn’t a crash on the horizon.

Read MoreFocus on Time in the Market, Not Timing the Market

Should you buy a home now or should you wait? That’s a big question on many people’s minds today. And while what timing is right for you will depend on a lot of other personal factors, here’s something you may not have considered. If you’re able to buy at today’s rates and prices, it may be better to focus on time in the market, rather than timing the market. The Downside of Trying To Time the Market Trying to time the market isn’t a good strategy because things can change. Here’s an example. For the better part of this year, projections have said mortgage rates will come down. And while experts agree that’s still what’s ahead, shifts in various market and economic factors have pushed back the timing of when that’ll happen. Here’s how that’s impacted homebuyers who’ve been sitting on the sidelines. As U.S. News says: “Those who put off buying a home during the past few years as they were holding out for lower mortgage rates have been left out of the market . . . mortgage rates have stayed higher for longer than previously expected, keeping monthly housing payments elevated. In other words, affordability didn't improve for those who chose to wait.” This is why timing the market may not pay off if you’re ready and able to buy now. The Proof Is in the Pudding: How Homeowners Benefit from Rising Home Prices Delaying your plans also means missing out on the equity you’d gain if you went ahead with your purchase today. And the potential equity gains that are at stake may surprise you. Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2028 (see the graph below): To give these numbers context, let’s take a look at a breakdown of what you stand to gain once you buy. The graph below uses a typical home’s value to show how a home could appreciate over the next few years using those HPES projections: In this example, let’s say you went ahead and bought a $400,000 home at the beginning of this year. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number. This data helps paint the picture of why time in the market really matters. The Advice You Need To Hear If You’re Ready and Able To Buy Now Right now, you may be focused on what’s happening with mortgage rates and how those impact your monthly payment, but don’t forget to factor in home prices. Prices are expected to continue climbing, just at a more moderate pace. And while a moderate rise in prices may not be fun for you now, once you own a home, that growth will be a huge perk. That’s the time in the market piece. Sure, you could try timing the market, but the equity you’ll be missing out on in the meantime is something to seriously consider. If you’re ready and able to buy now, you have to decide: is it really worth waiting? Rather than focusing on timing the market. It’s better to have time in the market. As U.S. News Real Estate sums up: “There's never a one-size-fits-all answer to whether now is the right time to buy a home. . . . There's also no way to predict precisely what the market will do in the near future . . . Perfectly timing the market shouldn't be the goal. This decision should be determined by your personal needs, financial means and the time you have to find the right home.” Bottom Line If you’re debating whether to buy now or wait, remember it’s time in the market, not timing the market. And if you want to get the ball rolling and set yourself up for those big equity gains, let’s connect to make it happen.

Read MoreWorried About Mortgage Rates? Control the Controllables

Chances are you’re hearing a lot about mortgage rates right now. You may even see some headlines talking about last week’s Federal Reserve (the Fed) meeting and what it means for rates. But the Fed doesn’t determine mortgage rates, even if the headlines make it sound like they do. The truth is, mortgage rates are impacted by a lot of factors: geo-political uncertainty, inflation and the economy, and more. And trying to pin down when all those factors will line up enough for rates to come down is tricky. That’s why it’s generally not worth it to try to time the market. There’s too much at play that you can’t control. The best thing you can do is control the controllables. And when it comes to rates, here’s what you can influence to make your moving plans a reality. Your Credit Score Credit scores can play a big role in your mortgage rate. As an article from CNET explains: “You can’t control the economic factors influencing interest rates. But you can get the best rate for your situation, and improving your credit score is the right place to start. Lenders look at your credit score to decide whether to approve you for a loan and at what interest rate. A higher credit score can help you secure a lower interest rate, maybe even better than the average.” That’s why it’s even more important to maintain a good credit score right now. With rates where they are, you want to do what you can to get the best rate possible. If you want to focus on improving your score, your trusted loan officer can give you expert advice to help. Your Loan Type There are many types of loans, each offering different terms for qualified buyers. The Consumer Financial Protection Bureau (CFPB) says: “There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.” When working with your team of real estate professionals, make sure you find out what’s available for your situation and which types of loans you may qualify for. Your Loan Term Another factor to consider is the term of your loan. Just like with loan types, you have options. Freddie Mac says: “When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.” Depending on your situation, the length of your loan can also change your mortgage rate. Bottom Line Remember, you can’t control what happens in the broader economy. But you can control the controllables. Work with a trusted lender to go over the things you can do that’ll make a difference. By being strategic with these factors, you may be able to combat today’s higher rates and lock in the lowest one you can.

Read MoreHow Many Homes Are Investors Actually Buying?

Are big investors really buying up all the homes today? If you’re trying to find a house to buy, this may be something you’re wondering about. Maybe you’ve read about it or seen reels on social media saying investors buying all the homes is making it even harder to find what the average buyer is looking for. But spoiler alert – there’s a lot of misinformation out there. To clear things up, here's the scoop on what's really happening. A lot of the big investor activity is actually in the rearview mirror already. The Wall Street Journal (WSJ) explains: “Investors of all sizes spent billions of dollars buying homes during the pandemic. At the 2022 peak, they bought more than one in every four single-family homes sold, though more recently their activity has slowed as interest rates rose and supply became tighter.” The key here is investor activity has slowed significantly, and even during the peak of investor buying, 3 out of every 4 single-family homes purchased were by regular, everyday buyers – not investors. And of the investors who bought over the past few years, most weren’t the big investors you may be hearing about. The vast majority were small mom-and-pop investors – people like your neighbors who own only a couple of homes, maybe even just their main residence and a vacation home. But let’s focus on the giant, mega-investor firms since that's what is being talked about so frequently on social media right now. Mega investors are those who own 1,000+ properties. You may be surprised to see that, according to the Wall Street Journal, they don’t buy all that many homes (see graph below): This graph tells us two things. First, institutional investors were never buying a large percentage of available homes. During the peak in 2022, they bought about 2% of available single-family homes. Second, that percentage has gotten even smaller recently (so small the number rounds down to 0%). In an effort to understand why that percentage is trending down, private lender RCN Capital asked investors about the challenges they’re facing. Here’s what Jeffrey Tesch, CEO of RCN Capital, found out: “Investors are already facing many challenges in today’s housing market – rising prices, limited inventory, and higher financing costs.” Understanding these challenges is important because they show big, mega investors aren’t taking over the housing market. So, don't fall for everything you hear. They aren't snatching up all the homes and making it impossible for regular people to buy. Bottom Line Big investors aren’t buying all the homes out there. If you've got questions about what you're hearing about the housing market, let's chat. I can help you understand what's really going on.

Read More

Categories

- All Blogs 197

- Affordability 18

- Agent Value 25

- Buying Tips 47

- Downsize 3

- Economy 16

- Equity 14

- First-Time Buyers 25

- Fishers 1

- For Buyers 117

- For Sale By Owner 4

- For Sellers 79

- Forecasts 8

- Foreclosures 5

- Home Prices 37

- Inventory 25

- Luxury/Vacation 2

- Mortgage Rates 45

- Move-Up 3

- New Construction 7

- Rent vs. Buy 7

- Selling Tips 41

Recent Posts