The #1 Thing Sellers Need To Know About Their Asking Price

When you put your house on the market, you want to sell it quickly and for the best price possible; that's generally the goal. But too many sellers are shooting too high right now. They don’t realize the market has shifted as inventory has grown. The side effect? Price cuts are on the rise, but t

Read MoreHere’s What a Recession Could Mean for the Housing Market

Recession talk is all over the news, and the odds of a recession are rising this year. And that leaves people wondering what would happen to the housing market if we do go into a recession. Let’s take a look at some historical data to show what’s happened in housing for each recession going all t

Read MoreNational Housing Trends To Watch

Nationally, the housing market has shifted over the last year. There are more homes for sale, price growth is moderating, and homes aren’t selling as fast. Do you want to know how our market compares? Let’s connect

Read MoreNational Housing Trends To Watch

At a national level, the housing market has shifted over the past year. There are more homes for sale, price growth has moderated, and homes are taking a little longer to sell. Do you want to know how our area compares? Let’s connect so we can go over what's happening locally and what this means fo

Read More4 Things To Expect from the Spring Housing Market

Spring is in full swing, and the housing market is picking up along with it. And if you’ve been wondering whether now is the right time to buy or sell, here’s the inside scoop on why this spring may be a great time to make your move. 1. There Are More Homes for Sale After a long stretch of tight

Read MoreRising Inventory Means This Spring Could Be Your Moment

Want to know two reasons this spring might finally be your time to buy? Inventory has grown and sellers may be more willing to negotiate as a result. That means you’ve got more options and more power than buyers have had in years. Let’s break it down. 1. You Have More Homes To Choose From The num

Read MoreShould I Buy a Home Right Now? Experts Say Prices Are Only Going Up

At one point or another, you’ve probably heard someone say, “Yesterday was the best time to buy a home, but the next best time is today.” That’s because nationally, home values continue to rise. And with mortgage rates still stubbornly high and home prices going up, you may be holding out for pri

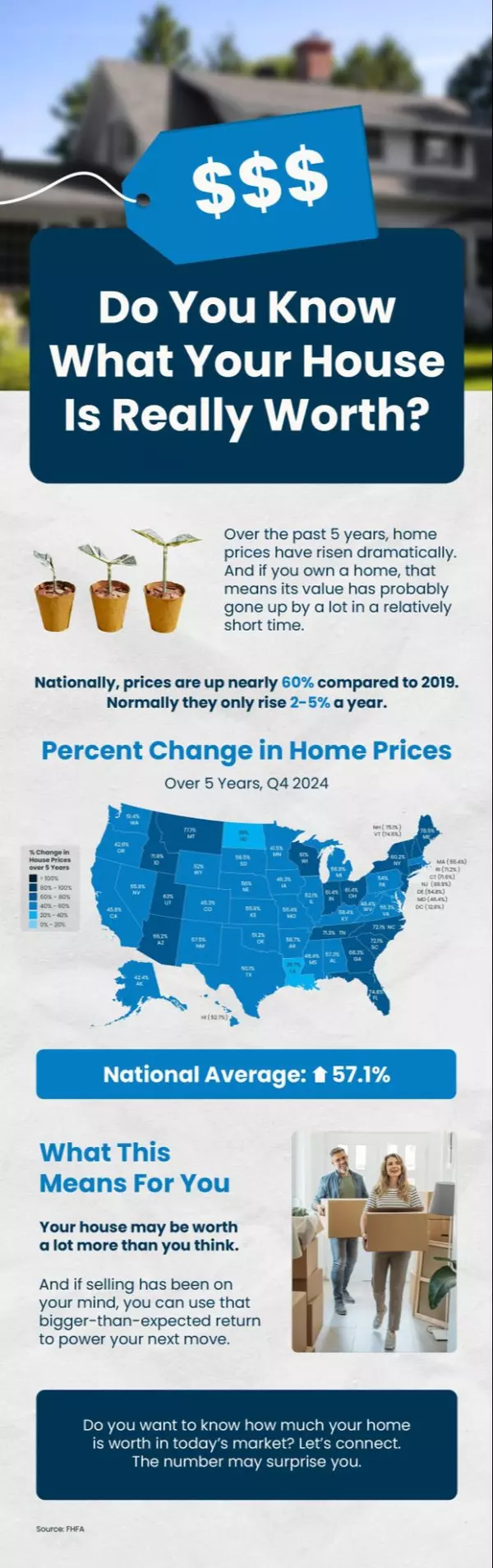

Read MoreDo You Know What Your House Is Really Worth?

Over the past 5 years, home prices have risen dramatically – and that means your home’s value has grown too. If you’re interested in finding out how much your home is worth in today’s market, let’s connect. The number may surprise you.

Read MoreDo You Know What Your House Is Really Worth?

Over the past 5 years, home prices have risen dramatically. If you own a home, that means your house may be worth a lot more than you think. Nationally, prices are up nearly 60% since 2019. And, if selling has been on your mind, you can use that bigger-than-expected return to power your next m

Read MoreDo You Know How Much Your Home Is Worth?

Over the past few years, you’ve probably seen a whole lot of headlines about how home prices keep going up. But have you ever stopped to think about what that actually means for your home? Home prices have risen dramatically over the past five years — far more than usual. And if selling has been

Read MoreBuying a Home May Help Shield You from Inflation

It feels like everything is getting more expensive these days. That’s because inflation has remained higher than normal for longer than expected – and that’s impacting the costs of goods, services, and more. And with rising costs all around you, you’re probably questioning: is now really the righ

Read MoreHome Price Growth Is Moderating – Here’s Why That’s Good for You

Over the past few years, home prices skyrocketed. That’s been frustrating for buyers, leaving many wondering if they’d ever get a shot at owning a home. But here’s some welcome news: that whirlwind pace of home price growth is slowing down. Home Prices Are Rising at a Healthy Pace At the national l

Read MoreThe Real Benefits of Buying a Home This Year

Have you been wondering whether you should keep renting or finally make the leap into homeownership? It’s a big decision, and let’s be real — renting can feel like the easier option, especially if buying a home feels out of reach. But here’s the thing: a recent report from Bank of America highlig

Read MoreTime in the Market Beats Trying To Time the Market

Time in the Market Beats Trying To Time the Market

Are you torn between whether to buy a home now or wait? Consider this. Forecasts show prices will climb for at least the next 5 years. If you wait, the price of a home will be higher later on. But, if you buy a $400K now, you could gain roughly $83K in equity as prices rise. If you're able to buy

Read MoreHow Home Equity Can Help Fuel Your Retirement

If retirement is on the horizon, now’s the time to start thinking about your next chapter. And you probably want to make sure you’re set up to feel comfortable financially to live the life you want in retirement. What you may not realize is you likely have a hidden goldmine of cash you’re not thi

Read More3 Reasons To Buy a Home Before Spring

Let’s face it — buying a home can feel like a challenge with today’s mortgage rates. You might even be thinking, “Should I just wait until spring when more homes hit the market and rates might be lower?” But here’s the thing, no one knows for sure where mortgage rates will go from here, and waiti

Read MoreSmaller Homes, Bigger Opportunities: The Homebuilder Trend Buyers Love

It’s no secret that affordability is tough with where mortgage rates and home prices are right now. And that may have you worried about how you’ll be able to buy a home. But, if you don’t need a ton of space, you may find you have more cost-effective options in an unexpected place: new home commu

Read MoreIf Your House’s Price Is Not Compelling, It’s Not Selling

There’s one big mistake you need to avoid when you sell your house this year: setting your price too high. It might seem like overpricing gives you room to negotiate or could really boost your profit, but the reality is, it usually backfires. In fact, Realtor.com says almost 20% of sellers — that

Read MoreWhen Is the Perfect Time To Move?

It’s easy to get caught up in the idea of waiting for the perfect moment to make your move – especially in today’s market. Maybe you’re holding out and hoping mortgage rates will drop, or that home prices will fall. But here’s what you need to realize: trying to time the market rarely works. And

Read More

Categories

- All Blogs 323

- Affordability 22

- Agent Value 41

- Buying Tips 85

- Downsize 4

- Economy 20

- Equity 24

- First-Time Buyers 47

- Fishers 1

- For Buyers 185

- For Sale By Owner 6

- For Sellers 124

- Forecasts 15

- Foreclosures 7

- Home Prices 64

- Inventory 43

- Luxury/Vacation 2

- Mortgage Rates 59

- Move-Up 3

- New Construction 8

- Rent vs. Buy 12

- Selling Tips 67

Recent Posts